by Nicholas Mitsakos | Book Chapter, Digital Assets, Investment Principles, Technology, Transformative businesses, Writing and Podcasts

Every industry consolidates to a handful of centralized competitors. That will never change regardless of current dreams of decentralization from Web 3.0. Modern computing is a constant struggle between decentralization and centralization. Centralization wins eventually, and it will again. These dynamics, combined with the latest crash that may cool investors’ appetite for all things crypto, suggest that Web 3.0 will not dislodge Web 2.0. Instead, the future may belong to a mix of the two, with Web 3.0 occupying certain niches. Whether or not people keep splurging on NFTs, such tokens make a lot of sense in the metaverse, where they could be used to track ownership of digital objects and move them from one virtual world to another. Web 3.0 may also play a role in the creator economy, assuring intellectual property ownership. NFTs make it easier for creators of online content to make money. In this limited way, at least, even the masters of Web 2.0 see the writing on the wall: on January 20th both Meta and Twitter integrated NFTs into their platforms.

by Nicholas Mitsakos | Book Chapter, Investment Principles, Writing and Podcasts

My new book, “Investment Principles: Strategies for an Irrational World” (Amazon link: Investment Principles: Strategies for an Irrational World.) looks at what’s really required for successful investing. While most authors try to give quick and effortless tips, I believe that a disciplined and methodical approach to investing is essential for true success. This means analytical work and an understanding that goes far beyond a simple summary description.

Successful investing requires understanding global economics, competitive, corporate, and micro-level analysis, game theory, and human emotions and behavior. That’s a lot to understand all at once but can be approached by segmenting each of these complex topics, giving sufficient depth to understand what is fundamentally going on in each area, and then, most valuably, show how these areas interact, enabling much more effective investment decision making.

The goal is to share an informed and distinctive way to think, predict the future with that combined information, and then make choices. Investment success combines predicting the future, the confidence to make bold choices, and the fortitude to stay with those choices.

by Nicholas Mitsakos | Book Chapter, Currency, Economy, Finance, Investment Principles, The Market, Writing and Podcasts

Financial markets are imbalanced and lack liquidity in crucial sectors, even historically stable and predictable markets such as the global bond and currency markets. Investments are slanted in one direction more frequently and the markets are vulnerable to big price swings as a result. These large global markets are not immune to ever more lopsided trades creating extreme volatility. This occurs even when a small change occurs in positions, sentiment, or news. Even the world’s most liquid markets, US dollar currency trades and US Treasuries, are seeing skewed positioning resulting in surprisingly large shifts in prices and Treasury bond yields. The market now leans too far one way or the other, and that imbalance will be forced to reverse more powerfully and unpredictably.

by Nicholas Mitsakos | Economy, Investment Principles, Investments, The Market, Writing and Podcasts

Investors expected that the Fed would not only end its bond buying program, but many believed it would also raise interest rates. While the Fed did agree to taper its bond buying, essentially decreasing its $150 billion monthly bond buying program by $15 billion per month, ending the program in 2022. However, the Fed kept interest rates the same and clearly signaled that it would not raise interest rates anytime soon, and almost definitely not until the taper of its bond buying was completed – in other words, not for at least one more year.

Investors who had been betting on the Fed raising interest rates wagered on the yield curve flattening for Treasuries. Therefore, they invested in short-term Treasuries believing those would outperform longer-term Treasuries, as well as 10-year and 30-year bonds. Instead, we are seeing the opposite happen. Short-term bonds are dropping in price and yields are approaching their highest levels since March 2020. Meanwhile, prices for long-term bonds have climbed. This same phenomenon is happening for government bonds that only in the United States, but also in the UK, Canada, and elsewhere.

by Nicholas Mitsakos | Book Chapter, Investment Principles, Writing and Podcasts

Failures are essential for success. The NASA flight director, Gene Kranz, who is famous for the Apollo 13 quote, “Failure is not an option” has been misunderstood. Mr. Kranz did not mean “don’t fail.” He meant was that there will be a solution, think boldly and courageously because, while the solution may not be obvious to you now, you will find it eventually.

Accepting failures is not accepting failure.

Failures – trial and error, unforeseen roadblocks, creative thinking, visions, and revisions that a minute will reverse – lead to insight, innovation, creativity, and unforeseen breakthroughs. That’s success.

Failure is when you stop.

by Nicholas Mitsakos | Book Chapter, Investment Principles, Investments, Writing and Podcasts

Distinguishing what’s happening in the market and the direction of important market metrics – the signal – from garbled, inconsistent, and mostly useless data – the noise – is extremely challenging today. Information is contradictory and transient making data and critical events more confusing and indistinguishable. Unusual circumstances brought about by the pandemic, subsequent supply chain interruptions, inconsistent production and demand, and unclear economic forecasts combined for almost unprecedented uncertainty and unpredictability.

Typically, near-term predictions are reasonable and reliable because we have immediately available and fairly accurate data making short-term predictions reasonably accurate. In other words, we can estimate what will happen because we have a good idea what just happened. But this is not the case today. Predictions based on the near-term past are more muddled now than ever. While we used to be able to say we can see a trend, whether that’s inflation, economic growth, or some other important metric, too much volatility, irrelevance, and lack of applicability (after all, who is going to project from a base that includes a pandemic impacting global supply chains and production?), we really can’t reasonably rely on any of that data to try to find a trend or connect the dots generating a near-term forecast with any meaningful depth of data and understanding

More intense volatility occurring more often will be characteristic of this market from now on. An investment strategy must withstand and profit from this. The only clear signal from the market is that there is far too much noise and not enough of a clear signal. Without clarity, determining an investment strategy is flying blind with no instruments.

Core holdings combined with an ability to withstand and profit from volatility and unpredictability are essential for investors today.

by Nicholas Mitsakos | Book Chapter, Investment Principles, Investments, Writing and Podcasts

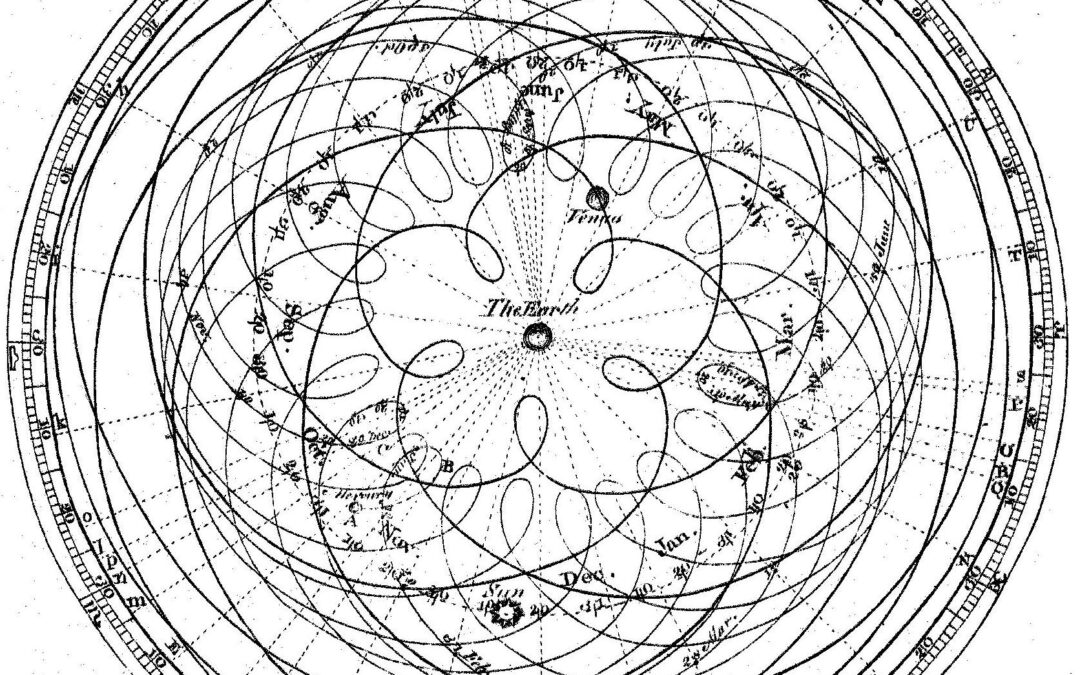

Assume nothing, new models and analytical tools, coupled with constant revision, questioning everything, reassessing, and re-analyzing, are essential to success in today’s markets. Often, and we are seeing that in today’s market, relying on bad assumptions, dogma, or prior belief can be disastrous.

This story about medieval astronomy applies directly to investment strategies, market valuations, and portfolio construction today. It’s the same lesson –begin by questioning the very assumptions on which an entire system is built. There is also a very specific application of this model that is particularly current.

One of the most valuable lessons is to assume no knowledge and analyze closely every initial assumption. Nothing is so obvious that it can’t be questioned. Unexamined ideas and assumptions will eventually be useless. Any assumptions and any model used to explain and predict anything (whether it’s the movement of planets or financial markets) needs to go back to first principles and discard any assumptions, preconceived knowledge, or bias.

by Nicholas Mitsakos | Book Chapter, Economy, Finance, Investment Principles, Investments, Writing and Podcasts

Economic predictions have always been highly variable and uncertain, and, for some reason, relied upon as if the future were a magical algorithm. Essentially, economists would make one fundamental mistake. They thought they were practicing a science. Data could be collected, inputted, and a predictive algorithm could be generated. Even Nobel Prize winners like Paul Samuelson believed that with enough data we could come to understand the economy and how it functioned.

This is nonsense. As Daniel Kahneman and Amos Tversky have shown us, human behavior and irrationality, combined with unpredictability and randomness (thank you Naseem Taleb) make this even a questionable social science. Using existing analysis and algorithms to reliably forecast is a fool’s errand, essential for someone’s tenure, and maybe even a Nobel Prize, but doesn’t add much that is useful. Some of the more laughable Nobel Prizes have been given to people who determined that markets were efficient. They are not. Economies can be predicted with useful data input. They cannot. A couple of inputs about inflation and the unemployment rate, and we know how to manage an economy. We can’t. That last one is the Philip’s Curve – true for a limited time and then it goes spectacularly wrong – a lot like most risk and market prediction models.

One thing we can add is that most predictions seem too good to be true, and almost always are. The economy is not a perpetual motion machine, nor is it a credit card with no limit and no requirement to pay the balance. The current notion that “deficits don’t matter” seems patently silly and naïve to think that we can simply print money without any economic discipline to generate sustainable profitable businesses with the efficient use of capital.

“Money goes where it’s needed, but it stays where it is treated well.”

Walter Wriston (former CEO of Citicorp)

That means it has to generate a return and not be co-opted by governments and public policy, nor be flooded by capital with no economic discipline.

Deficits may be a reasonable way to jumpstart a sluggish economy, but they are not sustainable. Current thinking is that fiscal discipline, debt repayment, and the idea of a balanced budget are anachronistic and useless. It is dangerous to stress test this idea because the downside is potentially cataclysmic. Capital likes a free market, but we hardly have a free market with money today. Constant stimulus does not create economic discipline.

by Nicholas Mitsakos | Book Chapter, Currency, Digital Assets, Investment Principles, Writing and Podcasts

“Distributed ledger technology and digital assets have the potential to dramatically disrupt global equity and debt markets.” (World Economic Forum, May 2021)

Distributed ledger technology (DLT), otherwise known as Blockchain technology, will radically simplify financial markets and, more importantly, fundamentally change the market’s infrastructure. Specifically, distributed ledger technology decentralizes critical data and enables an entirely new financial system where capital flows without the need for traditional intermediaries.

While there are challenges and numerous detractors, DLT is an irreversible disruptive force transforming capital markets and the global financial system.

Regulators (a potential obstacle) are increasingly comfortable with this technology. Distributed ledgers, decentralized finance, and Blockchain-based platforms are creating products and services evolving from exploration and experimentation to commercialization. DLT will be transformative to the world’s largest industry and represents an unprecedented opportunity. New digital platforms created by decentralized finance companies integrate securities and other digital assets comprehensively. The platforms enable market participants and intermediaries to issue, trade, settle, and provide custody services for digital assets, usually consisting of digitally native equity tokens (ICO’s).

These digital asset and financing platforms exist in parallel to existing market infrastructure and securities markets, in many cases offering an alternative digitized version of a standard asset class. Fundamentally, what is disruptive is that this new technology disintermediates all parties, creating effectiveness and efficiency in the transfer and recording of transactions that is unprecedented in legacy infrastructure

by Nicholas Mitsakos | Book Chapter, Investment Principles, Public Policy, Writing and Podcasts

Inequality is not an appropriate measure of economic performance or wealth creation.

Inequality is a relative and comparative statistic. It shows how wealth is distributed, which is not that meaningful, and certainly should not be the basis of economic policy. Essentially, inequality is a comparative metric and not an absolute one. That is, if everyone does better but a few people do much better, inequality increases, and this is seen as something bad even though everyone is better off. It is used to create misleading policies that focus on redistributing wealth that is created versus policy that should be focused on enabling greater and more distributed wealth creation – not wealth capture. Policy should focus on how to best create wealth for more people. The absolute degree of wealth creation is beside the point relative to other people. Creating opportunity for the most people is what matters.

As an example, overall wealth has increased over the last 30 years for every population group, but for the highest group, it has increased more substantially. But, why is that a problem? Instead, it is a natural and unavoidable outcome of the free market.

Here’s the analogy: if you want to hold a lottery, the prize has to be disproportionately large to have the most participants to raise the most capital. The simple goal is that net outflows (prizes) are smaller than the net inflows (contributions or purchased tickets). This is very similar to business opportunities and wealth creation.

As an economy, we want as many contributors to wealth creation – entrepreneurs and new businesses driving economic growth – as possible. The only way to do this is to enable market participants to have the greatest possible reward without restrictions. Most businesses will fail (much like most lottery tickets lose). But, because we have increased the number of willing participants, we also increase the opportunity to create the most wealth – the most businesses, jobs, and economic growth, as well as increasing the tax base from both businesses and individuals. So wealth creation, even if it is concentrated mostly in a handful of people, benefits the overall economy and society much more effectively than any attempt to limit that upside or redistribute it through politically popular but inefficient and demotivating policy.

by Nicholas Mitsakos | Book Chapter, Investment Principles, Writing and Podcasts

Risk is the permanent loss of capital.

It is not volatility, nor is it uncertainty. It is the realization of a loss. Therefore, risk is hard to understand because it is only clear with hindsight that a loss has occurred. Understanding how risk works can avoid this permanent loss by avoiding the mistakes that cause the permanent loss of capital.

Risk can also be used advantageously. Knowing that there is the prospect of loss, planning, and investment strategies that profit from these losses put you on the right side of the equation. Risk can be used to an investor’s advantage.

Essentially, anti-fragile (to coin Naseem Taleb’s term) strategies can benefit from volatility, uncertainty, and loss. Randomness permeates all markets, which means risk is always present. Knowing that, investment strategies need to be able to withstand unpredictable or unforeseen stresses. Not all risk factors can be known, or even if potential risks are identified, the magnitude and timing are unknown. What can be certain is that they will occur, and a portfolio that is “fragile” can be devastated

by Nicholas Mitsakos | Book Chapter, Investment Principles, Writing and Podcasts

Prepare for more frequent and extreme volatility. New and powerful influences, ranging from social media and financial technology to algorithmic trading and esoteric valuation models, will increasingly upset market stability and bring unprecedented rewards and unpredictable disaster.

Predictable market conditions will be upset by sudden unpredictable movements.

Financial markets can be predicted reliably only when the world does not change. Even during periods of stability, judgment based on expectations and assumptions as much as hard facts and economic analysis, form the basis for buying and selling decisions. Market crashes and financial crises are a continuing and breathtaking reminder that markets are irrational and uncertain. Taken to an extreme, the combustible combination disrupts global markets and societies. New analytical tools and technologies appear to make worrying about unforeseen risks obsolete. But this naïve belief in technology’s ability to understand and predict catastrophic risk is a fundamental cause of that very catastrophe.

Stability is illusory because in an uncertain world, unforeseen changes can have seismic effects. The pandemic is only the latest example, but there are always greater risks inherent in markets than is acknowledged, and most investment strategies do not accurately reflect the risk that certain investments are assuming for a given return. Safety can be an illusion if the risks are not well understood, both systemic and undiversified.

As we have seen, oversight, regulation, or any sort of self-imposed moderation will continue to be ineffective or nonexistent, and always trail behind the most dangerous and detrimental market developments. Financial weapons of mass destruction continue to multiply and are now available via smart phone in everyone’s pocket. Expect more and greater turbulence.